The main purpose of this ongoing blog will be to track planetary extreme, or record temperatures related to climate change. Any reports I see of ETs will be listed below the main topic of the day. I’ll refer to extreme or record temperatures as ETs (not extraterrestrials).😉

Main Topic: Rising Seas, Bigger Floods, and Other Increasing Climate Hazards Are Creating a Dangerous Instability in the U.S. Financial System.

Dear Diary. One of my greatest fears going through the 21st century is that climates changed weather will get so bad that the fabric of society will become unraveled due to high stress. People will look to the government and insurance companies for aid after surviving a climate crisis weather event, and that help may night come due to resources that are stretched too thin.

Already in the early part of the 21st century we see signs that the U.S. financial system is being stressed from the likes of Hurricane Ian making landfall in Florida last year, the historic western drought, and flooding around the nation. Dr. Jeff Masters recently wrote a well written deep dive into this subject, which I have permission to repost for today’s main subject:

Bubble trouble: Climate change is creating a huge and growing U.S. real estate bubble

Rising seas, bigger floods, and other increasing climate hazards have created a dangerous instability in the U.S. financial system.

by JEFF MASTERS

APRIL 10, 2023

When an ocean view is not a good selling point: storm surge from Hurricane Irene floods Nags Head, North Carolina, on August 26, 2011. (Image credit: Scott Olson/Getty Images)

Homes constructed in flood plains, storm surge zones, regions with declining water availability, and the wildfire-prone West are overvalued by hundreds of billions of dollars, recent studies suggest, creating a housing bubble that puts the U.S. financial system at risk.

The problem will get worse as sea level rises and storms dump heavier rains and if unwise building practices continue. But increased awareness of climate risks, more realistic flood insurance pricing, and reform of government disaster policy could reduce this overvaluation — and the risk of an economically disastrous bubble burst.

Climate futurist Alex Steffen has described the climate change–worsened real estate bubble this way: “As awareness of risk grows, the financial value of risky places drops. Where meeting that risk is more expensive than decision-makers think a place is worth, it simply won’t be defended. It will be unofficially abandoned. That will then create more problems. Bonds for big projects, loans and mortgages, business investment, insurance, talented workers — all will grow more scarce. Then, value will crash, a phenomenon I call the Brittleness Bubble.” Something that is brittle is prone to a sudden, catastrophic failure, and cannot easily be repaired once broken.

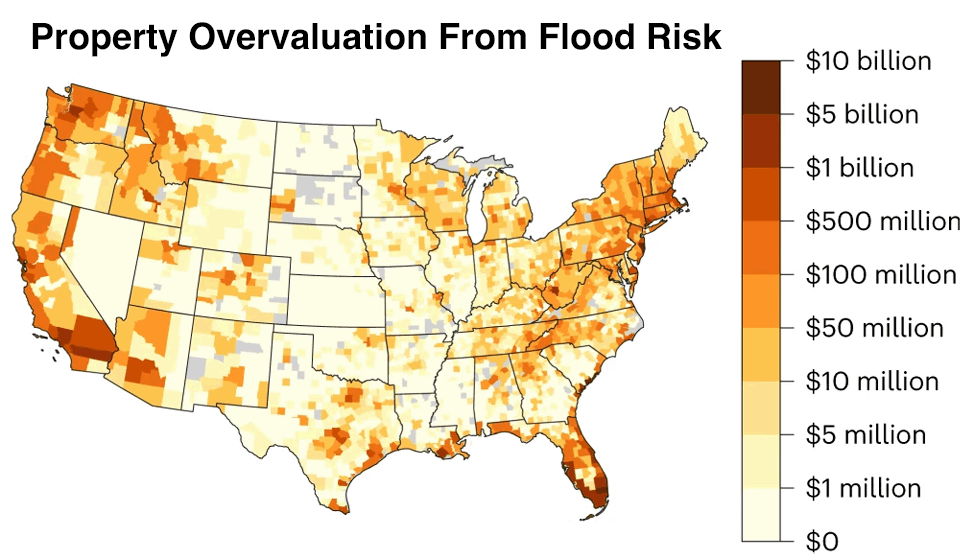

Figure 1. County-level overvaluation of property from flood risk. Florida had the highest property overvaluation — about $50 billion. In 2021, Florida’s real estate industry accounted for $294 billion, or 24% of the gross state product, according to a report from the National Association of Realtors. (Image credit: Gourevitch et al., 2023, Unpriced climate risk and the potential consequences of overvaluation in U.S. housing markets, Nature Climate Change volume 13, pages 250–257)

A housing bubble in the hundreds of billions of dollars

A 2023 study in the peer-reviewed journal Nature Climate Change has drawn attention to a massive real estate bubble in the U.S. — property that is overvalued by $121-$237 billion because of current flood risk. And that may be an underestimate.

A 2022 study by actuarial and consulting firm Milliman put a much higher price tag on this bubble — $520 billion, with almost 3.5 million homeowners facing a decrease in property value greater than 10% if flood risk were priced correctly. For comparison, the U.S. government spent $431 billion via the Troubled Asset Relief Program to help people recover from the 2008 housing crisis. In an interview last week with cnbc.com, one of the few skeptics who recognized the housing market was on the brink of collapse in 2007 — Dave Burt, CEO of investment research firm DeltaTerra Capital — agreed that a huge U.S. housing bubble existed because of unpriced flood risk. “We think of this repricing issue as maybe a quarter of the size and magnitude of the [global financial crisis] in aggregate, but of course very, very damaging within those exposed communities,” he said.

Increased flooding from climate change is worsening this overvalued property bubble. And such estimates don’t account for the effects of climate change-intensified wildfires, drought, and extreme heat. For example, the surge in catastrophic wildfires in California in recent years has contributed to a major affordable-housing and insurance crisis in the state. Lack of water in dry states with water availability issues, like Arizona and California, has also created increased risk of property overvaluation. In addition, a rise in extreme heat from a warming climate combined with a growing urban heat island effect is likely to make living in hot cities like Phoenix and Miami undesirable for an increasing number of people in coming decades, potentially depressing property values there.

Property overvaluation is particularly widespread among low-income households, which tend to be located in high-risk flood areas where land is cheaper. Poorer neighborhoods also receive fewer government dollars for flood protection infrastructure compared to wealthier neighborhoods, causing disproportionately high flood losses. If a crash in real estate values occurs, the U.S. wealth gap is likely to widen, because many households’ most valuable asset is their home.

Why is there so much development in risky places?

Jake Bittle’s must-read book, “The Great Displacement” (see my review) does a great job explaining why so many people live in high-risk flood areas:

For most of the preceding century, developers had been moving into floodplains, not out of them. Real estate tycoons in coastal states like New Jersey and Florida had erected thousands of houses on beachfronts and barrier islands, and engineers in inland areas had drained countless rivers and swamps to allow for construction on formerly uninhabitable land. The rapid pace of this construction was in part the result of ignorance about how floods worked, but it was also the result of an economic dynamic that sociologists call the “growth machine”: more construction meant more money for developers, more people living in waterfront towns and cities, and more tax revenue for local governments. A booming tax base allowed more spending on public services, which in turn attracted more people, created more demand for construction, and spread more money around. At least in the short term, everyone in a community won.

The federal government served as the de facto protector of this growth machine, a task it fulfilled through two major agencies. The first was the US Army Corps of Engineers, the nation’s principal builder of flood walls, levees, artificial beaches, and other structures that protected people from water. The other major player was FEMA, a younger agency that represented a mishmash of several different departments and distributed material aid after disasters. Both these agencies had always endeavored to keep flood-prone communities where they were, not move them elsewhere: the Corps wrapped levees and seawalls around existing towns to protect them from flooding, and FEMA stepped in after flood disasters to help people rebuild. This unspoken remain-in-place policy reflected the desires of the people who lived in these communities, most of whom had no desire to leave their homes, but it allowed residents of flood-prone areas to avoid bearing the burden of the risk they were incurring. If riverfront towns had had to finance their own levees and self-fund their own disaster recovery, their leaders might have thought twice about building next to the water, but that had never been the case. For as long as FEMA and the Army Corps underwrote the cost of living in risky places, whether through flood protection or post-disaster aid, vulnerable communities had both the incentive and ability to stay put.

In the 1960s, private insurers began pulling out of the flood insurance business, and it soon became clear that the unspoken remain-in-place model was unsustainable. As a result, the National Flood Insurance Program, or NFIP, was created. People who wanted to buy a home in a flood plain were required to get government flood insurance from NFIP (now administered by FEMA) in order to receive a federally backed mortgage. This approach was supposed to discourage people from moving into flood zones. But the price of the insurance was set too low, resulting in the government subsidizing people living in high-risk areas.

It wasn’t until 1989 that FEMA was finally allowed to stop exclusively rebuilding in the same place after a disaster, but instead prevent future flood losses by buying out properties that suffered repeated flooding. But buyouts comprise less than 20% of FEMA’s flood-risk reduction budget, and FEMA and Army Corps policies continue to encourage building in high-risk places.

The danger of the climate change–worsened real estate bubble

In part because of worsening climate change impacts, home insurers are already pulling out of the most at-risk areas, which has led to an insurance crisis in three states — Florida, Louisiana, and California. This insurance crisis threatens to make property ownership too expensive for millions, posing a serious threat to the economically critical real estate industry. Homebuyers who can’t afford insurance can’t get a mortgage, and in those fire and flood zones where insurance rates skyrocket, many owners will try to sell, potentially triggering panic selling and a housing market collapse like the crisis of 2008.

However, the 2008 crisis was relatively short-lived: Fixes to the financial system led to a rebound in property values after a few years. The climate change–induced housing crisis would likely be far worse because the underlying causes will worsen — sea levels will continue to rise, flooding heavy rains will intensify, and wildfires will grow more severe, increasing risk.

And as we saw during the Great Recession in 2008, a housing crisis can morph into a systemic financial crisis because banks own most of the value, and thus the risk, in housing and commercial real estate. A collapse in property values will also affect local governments that rely heavily upon property taxes to fund government services (Figure 2), forcing a cut in those services, and thus a further reduction in property values, in a vicious cycle. Property tax is the single largest source of revenue for local governments, accounting for 72% of tax revenues, on average. There are major state-by-state variations, according to the Tax Foundation — from as low as 40% in Alabama to as high as 98-99% in several states along the Northeast seaboard.

The 2023 study warned: “The collapse of housing prices during the Great Recession had negligible impacts on local government property tax revenues. In contrast, declines in property values due to climate risk are unlikely to be temporary, particularly for properties affected by sea-level rise … local governments may need to adapt their fiscal structure to continue to provide essential public goods and services.”

Figure 2. Local government vulnerability to revenue loss from unpriced flood risk. Orange hues indicate the proportion of municipal revenue derived from property taxes; purple hues indicate property overvaluation as a proportion of total property value (color breaks every 10%). Counties in black and outlined in red indicate municipalities that are both heavily reliant on property tax revenue and have high overvaluation. (Image credit: Gourevitch et al., 2023, Unpriced climate risk and the potential consequences of overvaluation in US housing markets, Nature Climate Change volume 13, pages 250–257)

Six actions that could help with the climate change real-estate bubble

1) Require sellers to fully disclose flood risks when selling a property.

The 2023 Nature Climate Change study found that in general, highly overvalued properties are concentrated in counties along the coast with no flood-risk disclosure laws. A prospective buyer who is informed of the flood risks of a property may be less likely to pay top dollar for it if the flood risks were high, reducing its overvaluation. Many states require a seller to detail the flood risk of any property being sold, and several more have implemented new disclosure laws in recent years. However, the powerful real estate industry often opposes these laws. The state with the highest amount of overvalued property — Florida — has no requirement to disclose flood risk (Figure 3).

Figure 3. The strength of flood risk disclosure laws by state as of 2022. States with weaker laws (e.g., Florida, Georgia, Alabama, and four states in New England) tend to have higher overvaluation of property from flood risk. Five states (Louisiana, Texas, South Carolina, Mississippi, and Delaware) have the most flood risk disclosure requirements. (Image credit: FEMA)

2) Increase climate change awareness.

Several studies have shown that less development occurs in high-risk areas where there is greater awareness of climate change. Climate change awareness has been increasing in recent years (see Tweet below), and the new floodfactor.com tool that rates property-specific flood, heat, wind, and wildfire risk from the nonprofit First Street Foundation has the potential to further increase awareness in the coming years.

Climate change awareness will likely continue to increase as climate change impacts accelerate and media attention grows, which should slow the growth of the bubble. However, a massive climate change denial campaign is being waged by the politicians, corporations, and media pundits who profit from maintaining the status quo. These rich and powerful interests are spending gargantuan amounts of money to convince people to ignore the climate change threat.

3) Charge market-based insurance rates.

The National Flood Insurance Program, or NFIP, has historically charged rates far lower than the actual flood risk. As a result, the program has experienced multiple taxpayer-funded bailouts, beginning in 2005 with Hurricane Katrina. NFIP is currently $20.5 billion in debt.

An NFIP reform implemented last year, Risk Rating 2.0, aims to change this problem by setting rates based on the risks at the exact location of a property. (This rate-setting formula has drawn considerable criticism, since it is partially based on proprietary data sets held by private companies, which prevents ratepayers from knowing the justification for their price changes.)

Risk Rating 2.0 has led to an increase in flood insurance rates for about 75% of all policyholders, which likely will reduce the size of the climate-related housing bubble. But rate hikes are capped at 18-25% per year, and it will take many years for Risk Rating 2.0 to charge fully realistic market flood insurance rates in some high-risk areas. For example, ratepayers in Louisiana will eventually see a 122% increase in premiums, according to Nola.com; in the Florida Keys, rates will at least triple in the long run.

NFIP rate hikes are causing homeownership to grow too expensive for some, particularly those with lower income, and a steady stream of people have been canceling their flood insurance policies in recent years (see Tweet below).

4) Reduce federal subsidies to live in risky places.

After catastrophic hurricanes like Katrina in 2005, Sandy in 2012, three category 4 hurricanes in 2017, and Ian in 2022, the federal government has stepped in to provide supplemental disaster relief money, largely through the public assistance sections of the 1988 Stafford Act. But as sea level rise expert Robert Young of Western Carolina University wrote in a 2022 New York Times Op-Ed:

Most of the funded projects are designed to protect existing infrastructure, in most cases with no demands for the recipients to improve long-term planning for disasters or to change patterns of future floodplain development. Outside of disaster aid, billions of dollars a year are spent by the federal government on resilience projects. The bipartisan infrastructure act of 2021 allocated some $47 billion over several years for resiliency. Most of the funded projects are designed to protect existing infrastructure, in most cases with no demands for the recipients to improve long-term planning for disasters or to change patterns of future floodplain development.

Major reforms to the Stafford Act and to government resilience infrastructure spending could help keep the climate-related housing bubble from expanding. But reform efforts face major challenges. According to an email from Dr. Samantha Montano, assistant professor in the Emergency Management Department at Massachusetts Maritime Academy, “there is a group of disaster researchers across disciplines eager to come together to write comprehensive policy reform. The type of reform that needs to be written is legally and ethically very complex. I estimate that at minimum it will take a year of us meeting regularly to write something that will be effective. Longer to negotiate it through various stakeholders. Our stumbling block has been a lack of political support and funding.”

In an interview in Gilbert Gaul’s excellent 2019 book, The Geography of Risk, former FEMA administrator Craig Fugate proposed, “Why not just stop writing [premiums] for new construction? If you build brand-new in a flood zone, you can’t buy insurance from the federal government. The private sector is going to write it.”

It would also make sense for NFIP to only provide insurance for primary residences. According to a 2013 study by the U.S. Government Accountability Office cited in The Geography of Risk, about 1/3 of the homes insured by NFIP were second homes or investment homes.

In a newsletter last week, Alex Steffen advocated that cities and regions must also be willing and able to “quickly ruggedize, innovate and change economic priorities to reduce risk and increase insurability, investability, and new development.” He lauded the White House’s new Economic Report of the President,which has a fantastic chapter, “Opportunities for better managing weather risk in the changing climate”, for having some bold-but-realistic Federal responses to climate risk.

5) Revamp FEMA and create a National Disaster Safety Board.

In its present form, FEMA is underfunded, understaffed, and has minimal authority. FEMA could be revamped and well-funded, becoming a cabinet-level organization.

In addition, a National Disaster Safety Board could advocate for policy changes that would correct bad development decisions, discriminatory policies, and lack of climate change planning.

6) Implement a fair and properly funded managed retreat policy.

Rather than rebuilding in areas of known hazard multiple times — a practice subsidized by taxpayers — we could instead get people out of flood zones and into affordable housing.

When will the bubble burst?

The inexorable rise in sea level alone increases the risk of a bubble burst unless radically transformative policies are enacted to reduce it.

NOAA predicts that sea level rise by 2050 for the U.S. will average 10-14 inches for the East Coast, 14-18 inches for the Gulf Coast, and four to eight inches for the West Coast. A rapid rise will continue thereafter, with NOAA estimating that the U.S. will experience four to seven feet of sea level rise by 2100, compared to 2000, in the intermediate and high scenarios.

But considering that people are continuing to flock to the climate-vulnerable Sun Belt states, we may still have a few years — and perhaps decades — before the bubble pops. One period of increased risk will likely occur in the mid-2030s, when a wobble in the moon’s orbit (part of a cycle that repeats every 18.6 years) will being unusually high tides to the U.S. Gulf Coast and West Coast, causing a surge in sunny-day high tide flooding. But given the highly concerning ramp-up in extreme weather in recent years, the housing bubble could burst sooner than that. Uncertainty has not been our friend when it comes to the impacts of extreme weather, which have largely been underpredicted by the climate models.

Politics, economics, and human behavior will greatly influence the timing of a burst, making the uncertainties extremely high. It could burst suddenly, causing a massive economy-shaking disruption, or more slowly, hitting sporadic high-risk or unlucky places, like a creeping metastatic cancer.

One thing is certain: The present-day trickle of Americans being displaced from high-risk areas because of climate change-worsened impacts is just beginning. In the future, millions of Americans could be displaced from their homes because of sea level rise and extreme weather by the end of the century, as Bittle explains in “The Great Displacement.”

There isn’t going to be an orderly transition to a new society that is in balance with the 21st-century climate; a massive climate-change disruption is already underway, and this great upheaval will fundamentally rip at the fabric of society. The sooner we acknowledge and plan for this reality, the less expensive and disruptive the transition will be, and the less suffering and death will occur.

Consider this vision for the future, though, from the excellent new book, “Charleston: Race, Water, and the Coming Storm,” by Susan Crawford: “Imagine planning for a multi-decade, gradual move, in consultation with each community, to new and welcoming locations well-connected to transit and jobs. Imagine caring for the least well-off among us, ensuring that they have a voice in this planning and choices about whether, when and how to leave, while firmly setting an endpoint on human habitation in the riskiest places.”

Related posts:

Book review: “The Great Displacement” is a must-read

Disasterology: a book review

With global warming of just 1.2°C, why has the weather gotten so extreme?

‘Is it foolish to hold onto my family’s beloved waterfront home?’

Recommended reading:

Gilbert Gaul’s 2019 book, The Geography of Risk

Alex Steffen’s newsletter

Bob Henson contributed to this post.

Website visitors can comment on “Eye on the Storm” posts (see comments policy below). Sign up to receive notices of new postings here.

JEFF MASTERS

Jeff Masters, Ph.D., worked as a hurricane scientist with the NOAA Hurricane Hunters from 1986-1990. After a near-fatal flight into category 5 Hurricane Hugo, he left the Hurricane Hunters to pursue a… More by Jeff Masters

Dr. Jeff Master’s Bubble trouble: Climate change is creating a huge and growing U.S. real estate bubblewas was first published on Yale Climate Connections, a program of the Yale School of the Environment, available at: http://yaleclimateconnections.org. This work is licensed under a Creative Commons Attribution-Noncommercial-No Derivative Works 2.5 license (CC BY-NC-ND 2.5).

Here are some “ET’s” recorded from around the planet the last couple of days, their consequences, and some extreme temperature outlooks, as well as any extreme precipitation reports:

Here is some more new March 2023 climatology:

Here is more climate and weather news from Wednesday.

(As usual, this will be a fluid post in which more information gets added during the day as it crosses my radar, crediting all who have put it on-line. Items will be archived on this site for posterity. In most instances click on the pictures of each tweet to see each article. The most noteworthy items will be listed first.)

If you like these posts and my work please contribute via the PayPal widget, which has recently been added to this site. Thanks in advance for any support.)

Guy Walton… “The Climate Guy”